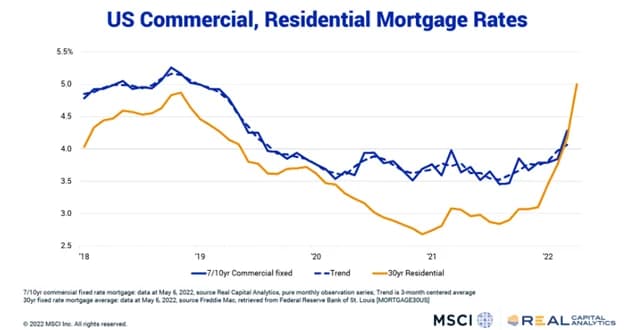

Global real estate 2026 mortgage rates: Trends and insights

Global real estate 2026 mortgage rates are shaping a complex, regional mosaic across housing and investment markets. As the year unfolds, lenders, buyers, and policymakers are all recalibrating around persistent rate levels that remain higher than pre-2020 norms in many markets, even as some regions see pockets of relief. In the United States, the 30-year fixed-rate mortgage has hovered around the mid-6% range into early 2026, testing affordability and buyer demand in a market already constrained by inventory and elevated prices. The Freddie Mac Primary Mortgage Market Survey (PMMS) shows the 30-year fixed at 6.11% as of February 5, 2026, with the 15-year rate at 5.50%. A year earlier, the 30-year rate was near 6.89%, underscoring a notable but incremental retreat from late-2025 highs. (freddiemac.com)

Across the Atlantic, mortgage-rate dynamics in Europe remain more accommodative than the US, reflecting ongoing monetary-policy normalization and credit-market transmission. The European Central Bank’s household borrowing data through early 2025 pointed to a euro-area composite rate for house purchases around 3.3%, illustrating the broad gap between European and American rate environments even as policymakers manage inflation and growth. In the United Kingdom, the Bank Rate sat higher than its pre-pandemic baseline, with typical fixed-rate products in early 2026 clustering around the mid-4% range for two-year and five-year terms, and the Bank Rate around 4.5% as policy calculations anticipated further adjustments. (ecb.europa.eu)

Beyond the US and Europe, mortgage-rate landscapes in other major markets reveal further divergence. In Canada, large Canadian lenders offered longer fixed-term rates around the mid-to-high 5% range for 5-year terms, with posted rates often above 6%, depending on loan-to-value and insurance requirements. In Australia, the Reserve Bank raised the cash rate to 3.85% in February 2026, signaling tighter conditions ahead than the earlier easing cycle, a move that typically translates into higher mortgage payments on new fixed-rate loans for some borrowers. These regional variations underscore the core reality of 2026: Global real estate financing is not a single-rate story, but a spectrum shaped by policy, credit markets, and currency dynamics. (forbes.com)

The year’s rate environment interacts with a broader housing-market backdrop that remains constrained by supply imbalances even as rates move lower from year-earlier peaks. Knight Frank’s global house price index and related analyses show that price momentum recovered modestly in late 2025, supported by easing monetary conditions in many markets, while affordability remained a pressing issue in a large swath of the globe. The latest Knight Frank data indicate that price growth picked up in several markets in 2025, but real affordability pressures persisted due to inflation and higher borrowing costs, a combination that is still reshaping buyer behavior and seller expectations in early 2026. (knightfrank.co.uk)

This piece provides a data-driven, neutral view of how Global real estate 2026 mortgage rates are influencing market trends, with concrete regional snapshots, real-world examples, and forward-looking guidance for businesses and consumers. The focus remains on technology-enabled market dynamics, policy impulses, and their implications for price trajectories, housing demand, and investment activity.

What’s happening across regions

US rate trajectory

The United States continues to operate in a high-but-plateau-rate regime. Freddie Mac’s PMMS data show the 30-year fixed-rate mortgage at 6.11% as of February 5, 2026, with the 15-year at 5.50%. This environment supports slower refinance activity, even as some improvement in affordability appears to be catching a portion of buyers back into the market during the spring season. A week-over-week view also shows slight declines from peaks reached late in 2025, but rates remain well above the sub-5% era many households recall from earlier in the decade. The persistence of elevated rates—paired with supply shortages and elevated home prices in many regions—continues to constrain overall buyer activity, though some markets are showing signs of tentative improvement as rates stabilize. (freddiemac.com)

-

Case study: US housing activity in early 2026 reflects a “recovery with caution.” January 2026 existing-home sales fell by 8.4% to 3.91 million, marking the slowest pace in roughly two years and the largest January year-over-year decline in several years. The drop occurred despite mortgage-rate relief versus late 2025, underscoring how inventory constraints and price affordability continue to cap demand. Median prices hovered near peak levels, illustrating a market where buyers face consistently high prices even as rates ease modestly. These dynamics were highlighted by the National Association of Realtors (NAR) data and reinforced by industry trackers. (nar.realtor)

-

Additional context: The broader US housing picture remains tethered to affordability, with ongoing inventory shortages capping the potential upside in activity. AP reporting noted that while rates had retreated slightly from late-2025 highs, the combination of high prices, a limited resale stock, and persistent affordability challenges continues to shape buyer intensity through early 2026. The spring home-buying season is pivotal for determining whether even modest rate relief can translate into meaningful demand growth. (apnews.com)

Europe and UK dynamics

European mortgage-rate dynamics present a contrasting narrative to the US, reflecting a relatively more accommodative borrowing environment due to ongoing monetary-policy transmission and strategic rate adjustments by the ECB. The ECB’s surveyed statistics through 2025 show that the composite cost of borrowing for house purchases in the euro area sits around 3.3% on average, with longer fixation periods generally carrying different rates. This lower-rate backdrop supports improved affordability relative to the US, though regional differences persist across member states, driven by local housing-market conditions and national credit regimes. Additionally, Bank of England communications through late 2025 and into 2026 emphasize continued pass-through of policy movements to mortgage products, with fixed-rate offerings in the 2–5 year ranges commonly landing in the mid-4% territory, depending on loan-to-value, term, and lender. This creates a broader regional spread in mortgage-cost dynamics between the US and Europe. (ecb.europa.eu)

-

UK case observations: By February 2026, UK mortgage-market data indicated ongoing competition among lenders, with two-year fixed-rate deals around the mid-4% range and five-year fixes slightly higher, illustrating the persistent uplift in borrowing costs relative to the strongest pre-2022 cycles but a notable improvement from the post-2023 peak. Analysts and lenders highlighted that the Bank Rate and market expectations for further policy moves were central to pricing in fixed-rate products. The UK market also saw expanded access to high-LTV deals for first-time buyers in early 2026, including near-95% LTV offers, albeit with common caveats and tighter affordability checks. (uswitch.com)

-

European-market context: Knight Frank’s global perspective underscores that Europe remains a center of price momentum in 2025, supported by easy monetary conditions in many markets and a broad-based European housing-market rebound. Yet, debt levels and policy-setting create a nuanced outlook for 2026, with some markets seeing limited price compression and others facing more pronounced affordability pressures. Knight Frank’s Global House Price Index and related commentary highlight the regional breadth of rate-driven impulses on demand and prices, even as yields and affordability remain varied across Europe. (knightfrank.co.uk)

-

US-Canada-Australia cross-border dynamics: In Canada, mortgage-rate environments remain elevated relative to the early-2010s, with five-year fixed deals often in the mid-to-upper 5% range or higher depending on product specifics, insurance, and lender criteria. Canada’s market has to contend with renewal risk for millions of borrowers facing higher payments as existing terms roll off. In Australia, the RBA’s February 2026 decision to raise the cash rate to 3.85% signals a more cautious, inflation-conscious posture and suggests higher mortgage payments ahead for new borrowers, even as the market benefits from improved labor-market dynamics in some regions. These regional nuances reinforce that Global real estate 2026 mortgage rates are not a single-rate phenomenon but a regional mosaic shaped by policy and credit-market structures. (forbes.com)

Why it’s happening: market forces and drivers

-

Central-bank policy trajectories and easing cycles: The late-2024 through 2025 easing cycle across major advanced economies supported a broad retracement in mortgage rates from their peaks, with North American markets seeing the most pronounced rate relief. Knight Frank’s analysis documents the pattern of multiple rate cuts through 2025 in several markets, even as the policy environment remained tight enough to constrain a full rebound in price and demand. In Europe, ECB transmission dynamics and the broadly softer inflation backdrop helped anchor mortgage costs at more moderate levels than those seen in the US. (knightfrank.co.uk)

-

Market structure and housing supply constraints: Inventory shortages persist in many regions, limiting the supply response to lower rates. US existing-home sales data for January 2026 show a sharp monthly decline, highlighting that even with rate relief, supply constraints and affordability pressures can hamper activity. The NAR release notes a 3.91 million SAAR pace, with inventory at ~1.22 million and a 3.7-month supply, signaling a market still calibrated toward sellers rather than buyers in many markets. The combination of rate relief and supply constraints continues to shape demand, pricing, and financing strategies. (nar.realtor)

-

Structural shifts in finance and tech-enabled services: The broader real estate services sector is navigating potential disruptions from AI and digital platforms. While AI-driven efficiency can reduce some operating costs and pricing pressures for service providers, the market’s reaction has been mixed, with European and U.S. property-services equities reacting to AI disruption concerns in early 2026. Analysts argue that the sector’s value remains tied to market expertise and the ability to manage complex transactions, even as automation reshapes some workflows. This dynamic intersects with mortgage-rate trends insofar as cheaper or faster services can influence closing costs and borrower experience. (theguardian.com)

-

Global capital-market dynamics: Real estate finance remains highly sensitive to currency movements, credit spreads, and cross-border capital flows. In major markets, broader risk sentiment, lender competition, and product innovation (such as more flexible fixed-term structures and higher-LTV offerings in some regions) influence how borrowers access financing as rates shift. For example, the UK market has seen expanding access to high-LTV products in early 2026, but with strong underwriting standards and program-specific conditions. (uswitch.com)

What it means: implications for business, consumers, and the industry

Business impact

-

Lenders and investors recalibrate pricing and product design: With mortgage rates in the mid-6% range in the US, and mid-4% in many European markets, lenders are balancing affordability with credit risk in their pricing, while seeking to preserve market share through innovation in product design, pre-qualification tools, and digital closing experiences. The Bank of England’s 2025–2026 policy communications emphasize pass-through dynamics and the need to manage higher payments for fixed-rate borrowers as deals come up for refixing. Capital-market outlooks from CBRE suggest that returns in commercial real estate will be driven more by income and asset-management excellence than by rapid cap-rate compression in the current cycle. (bankofengland.co.uk)

-

Investment activity adapts to interest-rate regime: CBRE’s US outlook in 2026 points to investment activity rebounding toward long-run averages, driven by income returns and asset-operator discipline rather than dramatic rate-driven price movements. European market outlooks highlight a similar emphasis on continued income generation and disciplined asset-management strategies, with long-term rates remaining elevated and liquidity conditions stabilizing gradually. This environment encourages targeted, evidence-based investment strategies and emphasizes the importance of data-driven underwriting, tenancy quality, and operational improvements. (cbre.com)

Consumer effects

-

Affordability and housing-ladder dynamics: Mortgage-rate levels continue to shape buyer eligibility, the demand for first homes, and the ability to refinance existing debt. In the US, even with rates easing modestly, affordability remains constrained by home-price levels and inventory shortages, which keep monthly payments relatively high and deter potential buyers. Housing-affordability indices in the US show improvement from the worst periods but still reflect a challenging landscape for many households. (globenewswire.com)

-

Market confidence and decision timelines: As rates stabilize near their peaks in some markets, buyers and sellers are adjusting expectations about price trajectories, listing timing, and the urgency to transact. In the UK, improved access to low-deposit mortgage options could facilitate more activity among first-time buyers, even as rates stay higher than historical norms. In the US, the spring home-buying season will be critical for assessing whether rate improvements translate into stronger close rates and more inventory turnover. (theguardian.com)

Industry changes

-

Real estate technology and services: The market is increasingly leveraging AI-enabled analytics and digital platforms to streamline property selection, pricing, and transactions. While AI brings efficiency benefits, the industry remains highly relational and transaction-heavy, with sophisticated due diligence and local-market expertise maintaining a premium. The threat and opportunity balance remains a topic of debate among investors and analysts, particularly in property-services sectors that have seen equity-price volatility tied to AI disruption concerns. (theguardian.com)

-

Policy and regulatory considerations: Policy-makers in the US, Europe, and the UK continue to shape mortgage markets through rate-path guidance, stress-testing frameworks, and consumer-protection rules. The Policy Reports from the Bank of England and ECB highlight that pass-through, underwriting standards, and fixed-rate dynamics will influence both the speed and the resilience of housing markets as rate cycles evolve. This regulatory backdrop matters for lenders’ willingness to extend credit, buyers’ access to affordable financing, and developers’ planning cycles. (bankofengland.co.uk)

Looking ahead: 6–12 month predictions, opportunities, and preparation

6–12 month outlook

-

US market trajectory: A 6.1%–6.5% range for 30-year fixed-rate mortgages in 2026 is plausible if inflation remains manageable and the labor market remains resilient. The January–February 2026 data show rates stabilizing near 6%, with occasional weekly fluctuations. Analysts from industry groups forecast a cautious path that could keep rates in the high 5% to low 6% range through much of 2026, unless inflation trends materially shift. For perspective, NAHB’s forecast pointed to the 30-year rate averaging around 6.17% in 2026, with a potential decline toward 6.0% in 2027 if conditions improve. This scenario would sustain affordability gains only if home prices decelerate or inventory improves. (fdmasia.com)

-

European and UK momentum: In Europe, mortgage costs are likely to remain among the more favorable axes of financing relative to the US, with euro-area rates around the mid-3% range for house purchases on average. The UK may see gradual rate relief as Bank Rate expectations shift and competition among lenders intensifies, potentially broadening access to fixed-rate deals for households while still keeping average rates above the pre-2020 baseline. The ECB’s and BoE communications through late 2025 and early 2026 suggest a path toward softer policy in some regions, albeit with caution given wage dynamics and inflation. (ecb.europa.eu)

-

Asia-Pacific and other markets: In markets like Australia, the February 2026 rate rise to 3.85% signals continued sensitivity to inflation and labor-market dynamics. With market participants pricing in potential further rate moves, new borrowers may face higher initial payments than mid-2025, though longer-term prospects will depend on inflation outcomes and housing supply. Investors and lenders in these markets will pay close attention to the RBA’s path and the resulting impact on housing finance and mortgage refinancing activity. (aussie.com.au)

Opportunities for borrowers, lenders, and developers

-

Refinancing waves and product innovation: As rates settle in a relatively narrow corridor, borrowers with maturing fixed-rate terms may look to refinance if their repayment burdens become manageable. Lenders can capitalize on this window by offering streamlined digital origination, rate-lock options, and alternative amortization structures that cushion payment shocks. The BoE and ECB policy communications emphasize that pass-through and affordability considerations will drive product design and consumer engagement. (bankofengland.co.uk)

-

Strategic markets and capitalization: For real estate investors, markets with stronger rent-to-price dynamics and favorable regulatory regimes may offer better resilience in a higher-rate environment. CBRE’s 2026 outlook for US and European real estate highlights income-driven performance and the importance of asset-management excellence, suggesting opportunities in value-add, density, and data-center-adjacent logistics, where demand remains robust despite macro headwinds. (cbre.com)

-

First-time buyer access and policy support: In regions like the UK, expanded access to high-LTV mortgage products could stimulate entry-level housing demand, counterbalancing affordability challenges. Policymaker attention to housing affordability and the stabilization of mortgage-market conditions will be a critical driver of demand-supportive measures in 2026. (theguardian.com)

How to prepare: concrete steps for readers

-

For borrowers: Monitor Freddie Mac PMMS updates for US rate direction, keep an eye on the housing market’s spring performance, and consider pre-approval or rate-lock strategies as you plan a purchase or refinance. The Freddie Mac data show the weekly rate hovering near 6% with small movements, underscoring the value of timely decisions in a dynamic rate environment. (freddiemac.com)

-

For lenders and developers: Emphasize data-driven underwriting, stress-testing under higher-rate scenarios, and asset-management excellence to sustain returns even when cap rates do not compress quickly. Central-bank communications suggest a cautious path, which means disciplined credit and disciplined pricing will be key to success in 2026. (bankofengland.co.uk)

-

For policymakers: Watch the transmission of policy actions into consumer borrowing costs, particularly fixed-rate mortgage pricing for households, and the impact on housing affordability. ECB and BoE policy notes emphasize the importance of rate-path clarity and its effect on household balance sheets. (ecb.europa.eu)

Comparison snapshot: global mortgage-rate landscape (selected regions, approximate benchmarks as of early 2026)

- United States: 30-year fixed-rate mortgage around 6.11% (PMMS as of 02/05/2026). This rate level remains elevated by historical standards and has a clear influence on affordability and refinancing activity. (freddiemac.com)

- United Kingdom: 2-year fixed around 4.85%; 5-year fixed around 4.94% (typical offerings in early Feb 2026); Bank Rate around 4.5%. A more accommodative environment than the US, but still meaningfully higher than the pre-2022 era. (uswitch.com)

- Euro area: Composite cost of borrowing for house purchases around 3.31% (household mortgage-rate statistics, euro area, early 2025 data; reflects broader euro-area conditions). (ecb.europa.eu)

- Canada: Five-year fixed posted rates around the mid-5% to low-6% range, with some variations by lender and product. (For a representative Canadian benchmark, see RBC-based posted-rate data in Forbes Advisor Canada coverage of RBC rates.) (forbes.com)

- Australia: Cash rate at 3.85% as of February 2026, with market pricing implying additional rate moves later in 2026; mortgage product pricing reflecting a tighter funding environment. This suggests higher initial payments for new borrowers relative to the 2024–2025 easing period. (aussie.com.au)

Note on data quality and future updates

- The numbers above reflect the latest credible sources available as of February 2026, including Freddie Mac PMMS for the US, central-bank reports and market commentary for the UK and euro area, and major market research firms for broader regional trends. Mortgage-rate figures can vary by lender, loan-to-value (LTV), down payment, and product type; readers should consult current, region-specific quotes for precise planning. Examples of ongoing, authoritative references include Freddie Mac PMMS, NAR and NAHB for US housing data, Bank of England and ECB policy communications, and CBRE/Knight Frank for market outlooks. (freddiemac.com)

Closing thoughts Global real estate 2026 mortgage rates remain a critical variable shaping housing demand, price dynamics, and investment strategies. The US shows a demand-limiting mix of elevated prices and tight supply even as rates ease modestly; Europe presents a comparatively more favorable financing environment but with regional disparities across member states. Other regions illustrate a broader spectrum of rate realities driven by local policy, credit markets, and currency effects. For policymakers, lenders, developers, and buyers, the path forward depends on vigilant monitoring of rate movements, inflation trajectories, and housing-supply responses—paired with nimble, data-driven decision-making to navigate the evolving terrain of the global mortgage-rate landscape.