Inflation path 2026 US: Data-Driven Insights

The Inflation path 2026 US is shaping up as a story of slowing price growth amid a still-volatile macro backdrop. For readers tracking technology and market trends, the data point out a tight balance: consumer prices are easing toward the Fed’s target, while wage dynamics remain resilient enough to sustain demand and, in turn, keep inflation expectations anchored. This opening era of 2026 is not about a dramatic collapse in prices but about how a broad mix of goods, services, and investment activity interacts with policy and productivity. The most surprising stat so far is the way sector composition within major benchmarks has shifted data-driven markets: the technology segment now commands a much larger share of market leadership than in recent cycles, even as inflation continues its gradual climbdown. In this piece, I lay out a curated set of 20+ statistics, each placed in clear thematic groups, with explicit context, sources, and implications for policy makers, investors, and business leaders. The data draw from the U.S. Bureau of Labor Statistics (CPI), the Bureau of Economic Analysis (PCE), and Fed-era projections, among other trusted sources, to give readers a grounded view of what’s driving the Inflation path 2026 US. The goal is to translate raw numbers into actionable implications for markets, technology investment, and policy considerations.

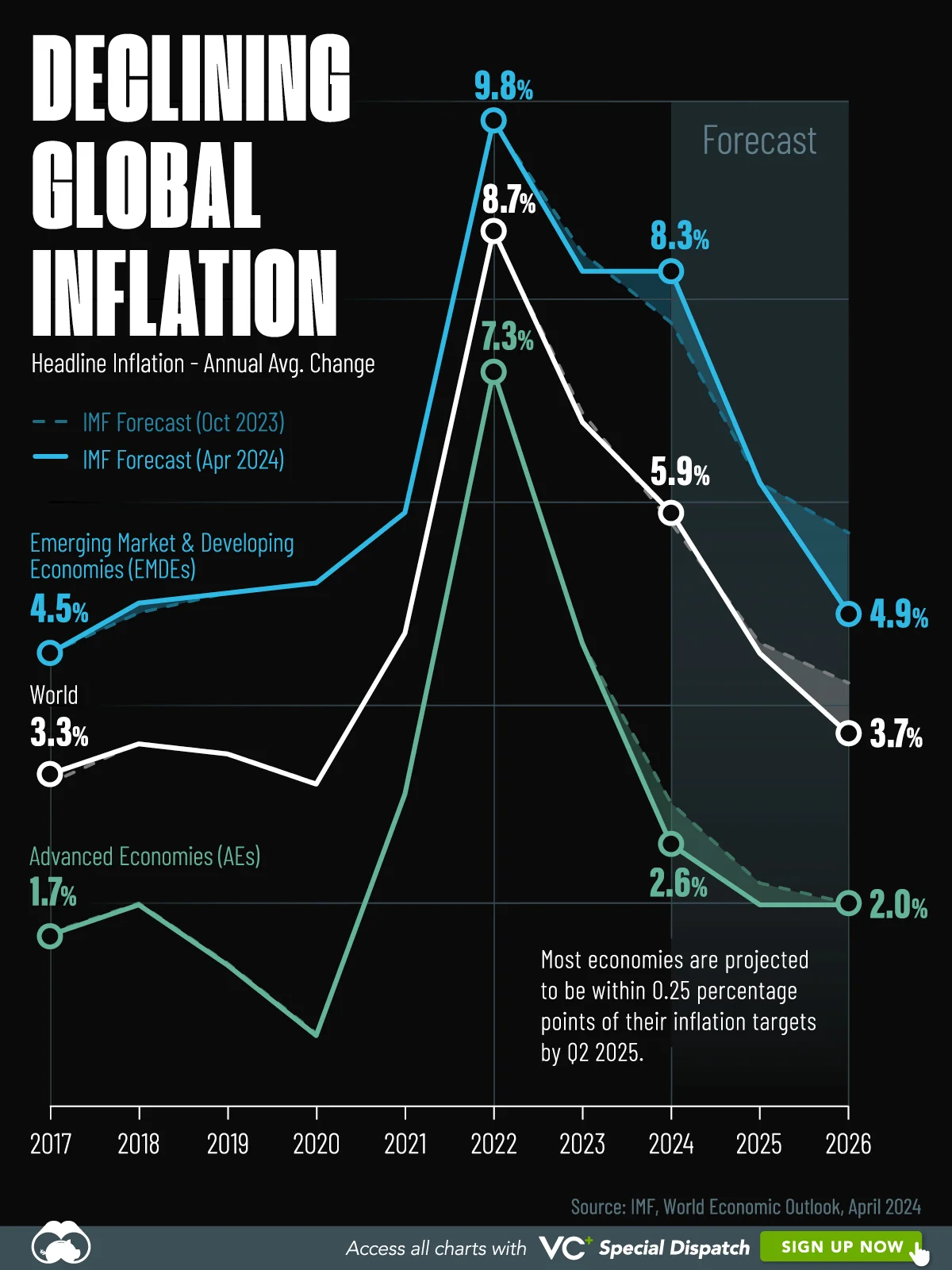

The opening data window for 2026 confirms a continued moderation in headline inflation, but it also highlights a still-heterogeneous price landscape. As of January 2026, the Consumer Price Index (CPI) rose 0.2% month over month, bringing the year-over-year rate to 2.4% for all items and 2.5% for core CPI, with shelter acting as a principal drag on overall inflation while energy prices softened. These cross-currents are critical for technology-driven market segments, where capex cycles, software pricing, and hardware costs all respond to price signals shaped by shelter, energy, and wage dynamics. The BEA’s PCE gauge, a broader measure of consumer inflation used by many policymakers, shows a still-favorable but not-quite-rapid enough pace to push inflation to zero or negative territory, underscoring the need for calibrated policy and corporate planning. Taken together, these data points sketch an inflation path that is easing toward target levels, yet remains susceptible to supply shocks and demand-side momentum from resilient labor markets. (bls.gov)

Price Dynamics Across CPI Components

All items CPI monthly change

- 0.2%: CPI-U rose 0.2% in January 2026 from December 2025 (seasonally adjusted). This monthly pace keeps inflation on a mild cooldown trajectory rather than a sharp drop. What it means: price gains are slowing enough to allow policy to assess the cumulative impact of prior rate moves while supporting consumer purchasing power. Source: BLS CPI News Release, January 2026. (bls.gov)

All items CPI year over year

- 2.4%: 12-month CPI for all items stood at 2.4% in January 2026, down from 2.7% in December 2025. What it means: the inflation engine is cooling, but not yet at the Federal Reserve’s 2% target, implying ongoing vigilance for both monetary policy and business pricing strategies. Source: BLS CPI News Release, January 2026. (bls.gov)

Core CPI year over year

- 2.5%: Core CPI (excluding food and energy) posted about 2.5% over the past 12 months in January 2026, with a monthly rise of 0.3%. What it means: underlying inflation pressures persist even as energy and food price volatility recede, highlighting areas where technology-enabled efficiencies and productivity gains could help compress services inflation over time. Source: BLS CPI News Release, January 2026. (bls.gov)

Shelter and housing components

- 0.2%: Shelter prices rose 0.2% month over month in January 2026, making housing the largest contributor to the month’s CPI increase. What it means: housing remains a sticky component of inflation; for technology-enabled housing services, rental analytics, and home-improvement markets, shelter dynamics will influence pricing power and consumer budgets through 2026. Source: BLS CPI News Release, January 2026. (bls.gov)

Energy prices

- -1.5%: Energy prices fell 1.5% in January 2026 (monthly). What it means: energy softness provides a cooling impulse to the overall CPI, potentially offsetting price pressures in durable goods and services tied to energy inputs. Source: BLS CPI News Release, January 2026. (bls.gov)

- -0.1%: Energy components were down about 0.1% on a 12-month basis as of January 2026. What it means: the energy drag has eased, supporting a more favorable inflation path for households and corporate cost structures reliant on energy intensity. Source: BLS CPI News Release, January 2026. (bls.gov)

Food prices

- 0.2%: Food prices increased 0.2% month over month in January 2026, with at-home and away-from-home categories rising at modest paces. What it means: food inflation remains manageable, reducing pressure on consumer disposable income and supporting consumer demand for technology-enabled goods and services. Source: BLS CPI News Release, January 2026. (bls.gov)

- 2.9%: Food at home prices rose about 2.1–2.9% year over year in early 2026 depending on subcategories, signaling that grocery channels still carry more persistent price pressures than general merchandise. What it means: food inflation’s persistence affects households differently than technology goods, informing hedging and pricing strategies for consumer tech in the retail channel. Source: BLS CPI News Release, January 2026. (bls.gov)

Used cars and other durable goods

- Decline in used cars and trucks price indexes: January 2026 saw declines in major indexes for used vehicles, contributing to softening inflation in a segment that was a notable driver of price gains in the mid-2020s. What it means: durable goods pricing dynamics, including electronics and software-enabled components, face lower price pressures than services in a mixed inflation environment. Source: BLS CPI News Release, January 2026. (bls.gov)

12-month inflation details by subcategory (Table cues)

- Energy: down 0.1% YoY; Electricity and other energy components show divergence across households and businesses, shaping consumer electricity bills and enterprise energy costs. What it means: volatility in energy subcomponents highlights the role of policy, commodity markets, and supply chains in inflation configuration. Source: BLS CPI News Release, January 2026. (bls.gov)

Themed Statistics: Inflation and Spending Signals

PCE price index and broader inflation metrics

- 2.8%: BEA’s Personal Consumption Expenditures (PCE) price index was +2.8% year over year as of September 2025. What it means: the PCE gauge, central to Fed policy discussions, remains above the 2% target but shows a slower pace than peak inflation, underscoring the potential for continued gradual disinflation into 2026. Source: BEA, Personal Consumption Expenditures Price Index. (bea.gov)

- 2.7–2.8% range: Throughout 2025 the PCE inflation rate hovered in the high 2% range as loose monetary policy and shifting consumer behavior evolved. What it means: policymakers watch this range to calibrate rate decisions and to assess how technology investment and productivity gains translate into lower inflation in the real economy. Source: BEA data releases and accompanying documentation. (bea.gov)

Personal Consumption Expenditures (PCE) price index: policy relevance

- Core PCE projections: In mid-2025, the Federal Reserve’s communications signaled core PCE inflation potentially moving toward the 2% target with a broad range of forecast paths for 2026. What it means: even with easing headline inflation, the core measure is the more relevant barometer for wage-price dynamics and business pricing power, including tech-sector pricing and services. Source: Federal Reserve Monetary Policy Report and related material. (federalreserve.gov)

Inflation expectations and policy signal framing

- Fed projections for 2026: Fed communications around mid-2025–early 2026 indicated a continued expectation of inflation converging toward the 2% target, with core PCE inflation projections often landing in a range near 2.0–2.4% by 2026 in many scenarios. What it means: this supports a cautious stance for investors in high-duration tech equities while keeping room for a measured rate path if disinflation continues. Source: Federal Reserve MPR materials and subsequent analysis. (federalreserve.gov)

The BEA PCE path and long-run inflation narrative

- 2.8% PCE path as a benchmark: The 2.8% figure for Sep 2025 remains among the more cited reference points for the broader inflation narrative, continuing to influence expectations about consumer demand and the pace of technology investment. What it means: a higher PCE reading relative to 2% can keep real interest rates elevated and support a more selective approach to tech capex and corporate pricing. Source: BEA PCE data release. (bea.gov)

Labor Market Momentum and Wages

Unemployment and payrolls

- 4.3% unemployment in January 2026: The unemployment rate remained at 4.3% in January 2026, with total nonfarm payrolls rising by 130,000 for the month. What it means: a still-tight labor market supports a steady consumer into 2026 and can sustain demand for tech-enabled services, while keeping wage growth from signaling an abrupt re-acceleration in inflation. Source: BLS Employment Situation News Release, January 2026. (bls.gov)

Labor force participation

- 62.5% participation: The civilian labor force participation rate stood at 62.5%, with the employment-population ratio around 59.8% in January 2026. What it means: participation trends matter for the inflation path because higher labor supply could relieve wage pressure and help cool services inflation, especially in tech-enabled industries with labor-intensive offerings. Source: BLS Employment Situation News Release, January 2026. (bls.gov)

Wages and earnings

- $31.95 average hourly earnings (Total private, January 2026): The January 2026 reading shows average hourly earnings at $31.95 in the private sector. What it means: wage growth persists at a pace that supports consumer demand but requires monitoring to prevent a wage-price spiral, particularly in sectors with high tech-adoption intensity. Source: BLS Employment Situation News Release, Table B-8. (bls.gov)

- $1,079.91 average weekly earnings (Total private, January 2026): The corresponding weekly earnings figure lands around $1,079.91. What it means: weekly earnings, in tandem with hourly wages, informs consumer purchasing power and financial conditions for households, affecting demand for technology products and services. Source: BLS Employment Situation News Release, Table B-8. (bls.gov)

Job growth and sectoral dynamics

- Health care and construction led January 2026 gains: Job gains were concentrated in health care, social assistance, and construction, while federal government and financial activities saw losses. What it means: sectoral shifts shape demand for technology-enabled productivity tools, healthcare IT, and construction tech, with implications for investment strategies across adjacent markets. Source: BLS Employment Situation News Release, January 2026. (bls.gov)

Long-term unemployment and resilience

- Long-term unemployed remain elevated: The number of people unemployed for 27 weeks or more hovered with notable year-over-year increases. What it means: persistent long-duration unemployment can pressure wage dynamics and consumer confidence, potentially affecting the Inflation path 2026 US through consumer spending and investment sentiment. Source: BLS Employment Situation News Release, January 2026. (bls.gov)

Patterns Section: What the Data Is Revealing

The inflation gradient across components is narrowing, but the pace varies by category

- The combination of 0.2% monthly CPI gains and a 2.4% YoY rate suggests price growth is decelerating but not uniformly across categories. Shelter remains a key driver of the monthly increase, while energy provides an offset with monthly declines. This pattern is consistent with a year in which demand remains resilient in services, yet energy and some goods pricing soften due to improving supply chains and lower input costs. Source: BLS CPI News Release, January 2026. (bls.gov)

Wage resilience supports continued demand for technology and digital services

- With unemployment around 4.3% and wages rising in the vicinity of 3%–4% annualized (as implied by hourly earnings and payroll growth), consumer demand for technology-enabled products and services remains robust. At the same time, core inflation around 2.5% signals that price discipline in services and goods persists, giving policymakers and firms a balanced backdrop for 2026 tech investments. Sources: BLS Employment Situation News Release, January 2026; BLS CPI News Release, January 2026. (bls.gov)

Market structure signals a tech-led leadership tilt

- The tech sector’s prominence in major stock market benchmarks is rising. As of late January 2026, the S&P 500 Information Technology sector accounted for about 34.6% of the index’s weight, with concentration of top holdings exceeding 40% of the benchmark. This signals a market environment where tech leadership has grown more concentrated, potentially amplifying market sensitivity to earnings surprises from a small set of large names. Implication: investors should consider balanced exposure and diversification within tech-adjacent segments, while policymakers watch the secular demand drivers behind AI and software investment. Sources: Nasdaq and S&P 500 sector data; Market commentary. (ycharts.com)

AI and productivity-driven demand as a structural impulse

- Market observers note an investment wave in AI and related software/hardware that has sustained elevated spending commitments, even as other inflation pressures ease. This has kept certain tech equities more reactive to earnings signals than to traditional macro indicators. Implication: technology companies with scalable AI-enabled platforms and enterprise software offerings may see continued pricing power, even as broad inflation cools. Sources: Market commentary and sector analyses (e.g., MarketWatch discussion on AI-driven demand and tech valuations). (marketwatch.com)

The policy anchor and market expectations: a cautious path toward 2%

- The Fed’s inflation projections in mid-2025 to early-2026 suggested inflation paths converging toward the 2% target, with core PCE remains a crucial gauge for policy and market expectations. This backdrop supports a measured approach to rate adjustments, while allowing markets to price in continued discipline around technology investment cycles. Sources: Federal Reserve Monetary Policy Reports and related analyses. (federalreserve.gov)

The BEA-PCE narrative complements the CPI picture

- While CPI provides a more immediate read on consumer price changes, the PCE price index offers a broader view of inflation across spending categories and consumer behavior. The YE 2025 PCE inflation pace around 2.8% highlights the convergence toward a target path, even as services inflation and durable goods costs interact with ongoing tech investment cycles. Source: BEA PCE data and documentation. (bea.gov)

A look ahead: implications for policy and markets

- For policymakers: the Inflation path 2026 US shows slowing inflation but persistent core pressures, underscoring the importance of data-driven policy calibration and clear communication about the trajectory to the 2% target. For markets: the tech sector’s weight and the concentration of leadership imply that earnings quality and AI-driven product adoption will remain key risk and opportunity drivers in 2026. For businesses: companies should plan for a gradual inflation environment, with cost containment in energy and shelter, and scalable technology investments that improve productivity in a still-tight labor market. Sources: BEA, BLS, and Fed projections; market analyses. (bls.gov)

The data-rich playbook for technology and market trends in 2026

- The data points above offer a data journalist’s playbook to assess the Inflation path 2026 US in a technology- and markets-focused lens:

- Monitor the CPI and PCE interaction to gauge where price pressures are most persistent (core services vs goods). Data: CPI YoY 2.4%; Core CPI YoY 2.5%; PCE YoY around 2.8% (as of 2025). Sources: BLS CPI, BEA PCE. (bls.gov)

- Track labor market momentum as a key inflation input. Data: Unemployment 4.3%; payroll gains 130k in January 2026; labor force participation 62.5%. Sources: BLS Employment Situation News Release, January 2026. (bls.gov)

- Assess wage trajectories in conjunction with inflation signals to forecast consumer demand for tech products and services. Data: Average hourly earnings $31.95; weekly earnings $1,079.91. Sources: BLS Tables in January 2026 release. (bls.gov)

- Consider market structure risks and opportunities arising from tech sector concentration. Data: IT sector weight ~34.6% of S&P 500 as of January 2026; top 10 holdings >40% of index. Sources: Nasdaq data and S&P sector analyses. (ycharts.com)

- Use the inflation path narrative to inform investment and policy timing around AI and software cycles, given the pace of disinflation and core-pce dynamics. Data: Fed projections and BEA-PCE context; 2.0–2.4% core PCE path ranges. Sources: Federal Reserve MPR, BEA, and related analyses. (federalreserve.gov)

Methodology and data sources

- The statistics presented here come from authoritative, primary sources:

- U.S. Bureau of Labor Statistics (CPI, unemployment, wages) for January 2026 and monthly trends. See CPI News Release, January 2026; Employment Situation News Release, January 2026. (bls.gov)

- U.S. Bureau of Economic Analysis (PCE price index) for inflation context and broader consumer inflation measures through 2025. (bea.gov)

- Federal Reserve policy communications for inflation projections and the policy framework guiding the Inflation path 2026 US. (federalreserve.gov)

- Market data and sector analysis for technology-driven market trends, including S&P 500 Information Technology sector weight, concentration in top holdings, and January 2026 milestone events. (ycharts.com)

Closing: Key takeaways from the data and how to use these insights

The Inflation path 2026 US narrative built from these data points is one of measured deceleration in headline inflation with persistent core pressures, a resilient labor market, and a technology-driven adjustment cycle in markets. The January 2026 CPI print shows a modest month-to-month rise, and the year-over-year rate remains above the 2% target but trending lower, signaling policy flexibility rather than urgency. Meanwhile, the PCE inflation picture, anchored by BEA data, suggests the broader inflation environment remains favorable for continued economic expansion, including in technology sectors that benefit from AI-driven productivity gains and digital transformation.

For readers and practitioners, the practical upshot is clear:

- Policy and market decisions should assume inflation will drift closer to 2% over the next 12–24 months, but not collapse; this implies cautious, data-driven rate normalization rather than abrupt policy changes. This stance matters for discount rates, capital allocation in tech, and corporate investment in AI and software. Sources: BEA, Fed projections. (bea.gov)

- Tech investment remains a principal driver of growth, with market leadership increasingly concentrated in a handful of Information Technology names. Investors should balance the potential for outsized returns from AI-enabled platforms with diversification to mitigate idiosyncratic risk. Sources: Nasdaq/Market data; S&P sector composition. (ycharts.com)

- The labor market’s resilience—low unemployment and solid wage growth—continues to support consumer demand for technology-enabled goods and services, even as inflation moderates. This dynamic argues for a nuanced approach to price setting and capex across tech-enabled sectors, including software as a service, cloud computing, and AI tooling. Sources: BLS unemployment and wages data. (bls.gov)

As the year unfolds, the Inflation path 2026 US will be defined by how quickly core inflation cools, how wage dynamics evolve in a still-tight labor market, and how the technology sector navigates a market that remains highly sensitive to earnings signals from leading firms. The data indicate a cautiously favorable environment for both policy normalization and technology-driven growth, but with enough ambiguity to warrant ongoing scrutiny of inflation metrics, wages, and market leadership shifts. For Wall Street Economicists readers seeking to understand the trajectory, the essential message is: follow the data, watch the core inflation signal, monitor labor market momentum, and stay attuned to the technology sector’s evolving market structure. The path ahead is not a straight line to 2%; it’s a guided, data-informed journey through a landscape of gradual disinflation, opportunistic tech investment, and policy prudence.