U.S. inflation 2026 January: Trends & Impacts

The January 2026 inflation picture arrived with a familiar tone: price pressures cooled modestly, but real-world effects remain uneven across goods and services. For readers watching technology markets and the broader economy, the January read provides a critical datapoint about the pace of disinflation and what it may mean for pricing power, consumer demand, and investment strategy. The Bureau of Labor Statistics’ CPI release shows a headline that moved at a modest pace, while shelter-driven dynamics and energy volatility continued to shape the monthly and year-over-year numbers. These details matter now because the inflation path helps set expectations for monetary policy, consumer spending, and corporate pricing decisions in tech-heavy sectors. In particular, the January 2026 data point to a selective easing in inflation that could influence the Fed’s near-term posture, investor risk appetite, and how tech firms price AI-enabled products and services in a volatile macro backdrop. The consensus around the January CPI has also influenced expectations about the longer-term inflation trajectory, with market surveys showing a drift lower in near-term inflation expectations even as longer horizons remain more anchored around the 3% range. (bls.gov)

Looking ahead, analysts note that the inflation picture is not uniform. The January 2026 CPI report indicates a 0.2% month-over-month increase in the consumer price index for all items (seasonally adjusted), with a 12-month change of 2.4%. This moderation follows a higher pace in late 2025 and reinforces a narrative of disinflation, albeit uneven across categories. For technology markets, a slower overall inflation pace can support a more predictable pricing environment for software, hardware, and cloud services, even as certain cost components—like shelter and some services—remain sticky. Analysts at market data providers and think tanks have signaled that January's numbers could tilt expectations toward a cautious stance on policy normalization, while acknowledging that core inflation remains a focal point for policymakers. (bls.gov)

This piece provides a data-driven trend analysis tailored for Wall Street Economicists’ readers: a neutral, information-rich look at what U.S. inflation 2026 January means for technology and market trends. We begin with a precise accounting of January’s numbers, then unpack the market mechanics behind them, and finally translate those forces into business implications, consumer effects, and near-term opportunities for tech-focused players.

What’s Happening in January 2026

Headline Metrics

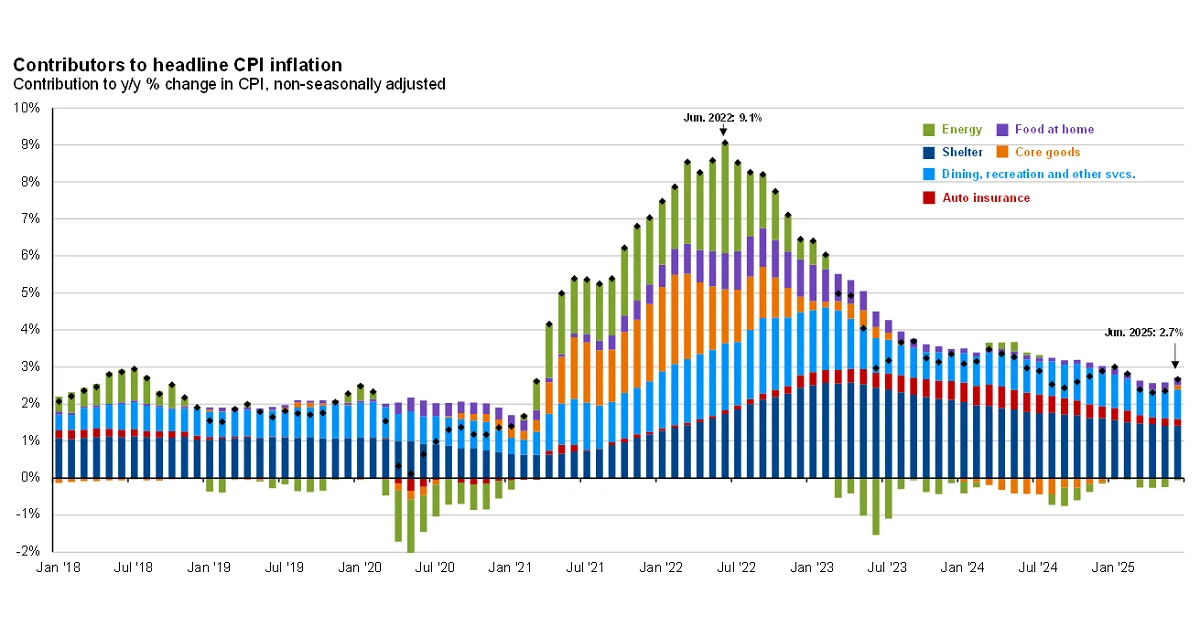

- The CPI-U increased 0.2% on a seasonally adjusted basis in January 2026. Over the last 12 months, headline inflation stood at 2.4%. These figures are the key yardsticks for investors and executives monitoring the speed of price gains and the risk of price shocks returning. (bls.gov)

- The all-items index rose 2.4% year over year for January, reversing a slower Dec-year pace and underscoring the continuing but easing inflation path that policymakers and markets are interpreting in real time. (bls.gov)

Core vs Headline Dynamics

- The “all items less food and energy” index rose 0.3% in January, highlighting that underlying inflation—where demand and services price pressure are more persistent—remains a central consideration for the Fed and for corporate pricing decisions, especially in services and AI-enabled offerings. This separation between headline and core inflation is a critical signal for tech firms navigating service-based revenue and subscription models. (bls.gov)

Price Drivers and Sectoral Dispersion

- Shelter costs were the largest contributor to the monthly increase, rising 0.2%. In contrast, energy fell 1.5% for the month, reflecting the ongoing energy-price dynamics that often cushion overall inflation even as other components rise. Food rose 0.2% overall, with food at home up 0.2% as well. These component moves illuminate where price pressures are intensifying and where relief is most visible for households. (bls.gov)

- Within the subcomponents, the shelter and rent-related indices (owners’ equivalent rent, etc.) continued to show resilience, underscoring a structural lag in housing-related costs—a phenomenon that has broad implications for consumer budgets and the pricing power of services-oriented sectors, including tech-enabled services. (bls.gov)

Real-World Snapshots (2 Case Studies)

- Case Study 1: Memory Chip Shortage and PC Price Pressures. A global memory shortage has amplified costs for DRAM and NAND, pressuring PC OEMs and consumer devices to reprice or trim specifications. Industry reporting indicates significant price increases in memory components and related devices as AI infrastructure demand remains robust, with implications across OEMs like Dell, Acer, Xiaomi, and LG. This dynamic helps explain observed price moves in consumer hardware and the broader tech supply chain during late 2025 and early 2026. (wsj.com)

- Case Study 2: Memory-Cost Pressures on Routers and Set-Top Boxes. The memory-cost surge has also flowed into the cost structures of consumer networking gear and set-top devices, with reports noting several memory-driven price increases in ISP-provided routers, gateways, and STBs. The effect on hardware pricing aligns with broader inflation dynamics discussed in January 2026 CPI analyses and suggests ongoing pressure on hardware margins in 2026. (tomshardware.com)

Table: January 2026 CPI Snapshot (selected components) | Component | January 2026 Change (MoM) | 12-Month Change | Notes | | All Items | 0.2% | 2.4% | Seasonally adjusted; headline figure | | Shelter | 0.2% | (varies by subindex) | Largest contributor to month’s rise | | Food | 0.2% | 2.9% | Food at home +0.2%; food away from home +0.1% | | Energy | -1.5% | -0.1% (overall energy) | Gasoline notable drop; energy prices volatile | | All items less food and energy | 0.3% | 2.5% | Core inflation metric remains sticky |

Notes: The data above reflect the Bureau of Labor Statistics’ January 2026 CPI release and related breakdowns. Shelter, energy, and food components are among the most influential monthly movers. Core inflation excludes food and energy. (bls.gov)

Who’s Affected

- Households with heavy housing costs feel the shelter-driven portion of inflation the most. Rent and owners’ equivalent rent continued to exert outsized influence on the monthly CPI move, underscoring how housing affordability remains a major budget concern for many families, even as some goods prices ease. (bls.gov)

- Consumers facing large discretionary purchases in tech hardware (PCs, memory-driven devices, routers, and set-top devices) are affected by the memory-price cycle described above. As memory costs rose through late 2025 and into 2026, bill-of-materials pressures translated into higher or less-flexible pricing for consumer tech hardware. (wsj.com)

- Business-to-business tech buyers—especially SaaS and AI-enabled software—may experience a combination of softer macro inflation and price retention on high-value services, given core inflation’s stickiness in services and software prices, which can inform renewal strategies and contract terms. Market surveys and inflation expectations data suggest a cautious stance on near-term inflation, which could influence procurement and budgeting for enterprise software. (newyorkfed.org)

Why It’s Happening

Demand, Labor, and Service-Driven Pressures

- Inflation dynamics in January 2026 reveal that core services and shelter-driven components continue to exert upward pressure, consistent with a labor market that remains resilient but with ongoing costs in housing services. This pattern aligns with the broader view that disinflationary progress is uneven, particularly in housing and services where price transmission can lag behind goods. The contrast between goods price relief and persistent services inflation is a core feature of the current inflation landscape. (bls.gov)

- Inflation expectations data from the New York Fed’s January 2026 survey show a modest improvement in short-term inflation expectations (one-year ahead) even as longer horizons remain anchored around target levels. This dichotomy—cooler near-term expectations with persistent longer-term concerns—helps explain why financial markets are parsing the January numbers for signals about Fed policy timing and the sustainability of price relief. (newyorkfed.org)

Supply Chains, Energy, and Commodity-Cycle Dynamics

- Energy prices pulled back in January, contributing to the softer year-over-year pace. Gasoline, electricity, and other energy subcomponents exhibited differing trajectories, illustrating how commodity cycles can dampen or amplify headline inflation in the short run. In an economy where energy is a lever for inflation, these movements can influence consumer spending patterns and corporate energy costs—particularly for tech and data-center operations that consume sizable energy inputs. (bls.gov)

- The memory-chip supply dynamics that dominated consumer-tech pricing in 2025 continued to reverberate into early 2026, underscoring how supply constraints in semiconductors feed into pricing decisions across hardware ecosystems. The WSJ and industry reports point to memory-price pressure that affects PC OEMs and peripheral devices, a trend that aligns with the broader inflation narrative and has implications for consumer tech affordability and product configurations. (wsj.com)

Industry Factors and Policy Context

- Monetary policy expectations hinge on inflation trajectories. With January CPI showing a slower pace of inflation but still above a level consistent with a full return to 2% in the near term, markets expect a cautious Fed stance. This environment encourages firms to manage pricing with a focus on value, productivity, and efficiency, rather than broad, aggressive price increases. Market observers have highlighted that the Fed’s next moves will be data-dependent, with disinflationary signals in housing and services playing a crucial role in policy deliberations. (bls.gov)

What It Means for Businesses, Consumers, and Technology

Business Strategy and Pricing Discipline

- For technology firms, the January 2026 inflation print reinforces the importance of disciplined pricing, especially in AI-enabled software and services where value-based pricing and tiered models can help protect margins in a disinflationary environment that is still uneven. Industry analyses suggest that pricing discipline and structured deal governance tend to outperform peers in environments with persistent inflation at the service level. As software pricing continues to evolve—especially with AI features embedded in core offerings—expect continued emphasis on price clarity, renewal uplifts, and value-based pricing strategies. (baringa.com)

- The memory-cost pressures highlighted by recent reports also imply that hardware pricing and supplier negotiations remain critical for hardware-centric tech players and OEM ecosystems. Firms may pursue longer-term supplier contracts, hedging strategies, or product-tier adjustments to balance margins with consumer affordability. Case studies from the memory-price cycle illustrate how supply constraints translate into both price changes and product-level adjustments. (wsj.com)

Consumer Effects and Budgeting

- For households, the shelter-driven inflation signal underscores ongoing housing-cost considerations even as other prices soften. This reinforces the need for prudent household budgeting around housing, utilities, and related services, while some non-housing categories, including certain tech devices, may see less aggressive price pressure as the inflation path evolves. The January numbers thus point to a mixed consumer environment: some pockets of relief (energy), some persistent pressure (housing and services). (bls.gov)

Industry Changes and Adaptation

- The tech ecosystem is likely to respond to inflation signals with a continued emphasis on efficiency, optimization of cloud spend, and smarter product pricing strategies. In addition, the memory-cost dynamic may push hardware vendors to adjust product specs, pricing, and go-to-market approaches to balance demand with supply realities. The broader inflation backdrop also adds impetus for software and AI-driven cost savings that can offset hardware price pressures for enterprise customers. (wsj.com)

Looking Ahead: 6–12 Month Projections and Opportunities

Near-Term Inflation Trajectory

- If January’s 0.2% monthly rise and 2.4% year-over-year pace hold, the path of inflation remains on a slower but persistent trajectory. Analysts expect the pace of disinflation to continue, though the rate of improvement may hinge on housing costs, wage dynamics, and external shocks. Market consensus and financial-news commentary point to a cautious expectation of a measured path toward the Fed’s target, with policy moves data-dependent and slow to pivot while inflation indicators improve. This context matters for tech investment and pricing strategies, where financial planning relies on a predictable macro backdrop. (bls.gov)

Opportunities for Tech Firms

- Value-based pricing for AI-enabled tools and cloud services could become more widespread as firms seek to align price with measurable value and outcomes, especially in a climate where inflation expectations have cooled but core services inflation remains elevated. The tech sector may benefit from disciplined pricing that emphasizes ROI, productivity gains, and user adoption metrics. Market outlooks and advisory analyses indicate a growing emphasis on structured pricing programs and governance to protect margins in a high-cost environment. (baringa.com)

- Given memory-cost pressures in hardware ecosystems, opportunities may arise for memory-efficient architectures, alternative memory tiers, and design optimizations in consumer and enterprise devices. Suppliers and manufacturers could pursue long-term supply contracts and strategic sourcing to mitigate volatility, with potential downstream effects on device pricing and feature sets. Industry reporting on memory dynamics supports this narrative and highlights the broader supply-chain implications for hardware-driven segments of the tech market. (wsj.com)

6–12 Month Preparations for Investors and Executives

- Investors should monitor the inflation path for signals about the timing of policy normalization and how it affects discount rates, corporate earnings, and capital spending in technology. The New York Fed’s inflation expectations data provide a useful baseline for sentiment around one-year horizons, while longer-horizon expectations remain rooted in structural factors such as wages and housing costs. This dual signal suggests a cautious but opportunistic stance for tech equities tied to software, AI, and cloud services. (newyorkfed.org)

- Corporate finance teams should incorporate a scenario-based approach to pricing and procurement, given the uneven inflation dynamics. Scenario planning can help optimize pricing bands, renewal strategies, and cost-management initiatives in both software and hardware product lines. Industry research points to the growing importance of value-based pricing and structured contracting as levers to sustain margins in a fluctuating inflation regime. (baringa.com)

What to Watch Next

- January 2026’s inflation mix emphasizes shelter and services persistence even as goods inflation softens. The next several CPI readings will be crucial for confirming whether the early-2026 disinflation trend broadens beyond durable goods into services. Watch for shelter price dynamics, core inflation progress, and energy price reversal or stabilization, as these will shape Fed policy signals and business planning in tech-heavy industries. Market commentary and government data releases will continue to provide the essential inputs for this assessment. (bls.gov)

Closing

The January 2026 CPI release confirms a cautious but meaningful step toward disinflation, with a 0.2% monthly increase and a 2.4% year-over-year rate. For technology markets, the data underscore a nuanced environment: cooling headline inflation supports a more stable pricing and planning backdrop, yet shelter-driven costs and persistent service-price momentum keep risk and uncertainty in play. Case studies from memory-cost dynamics illustrate how supply constraints can translate into real-world pricing and product-design decisions that reverberate through consumer hardware and enterprise tech ecosystems. As Wall Street and corporate boards adjust to this environment, the most resilient players will combine disciplined pricing, efficiency gains, and a tested capacity to translate AI-enabled value into tangible returns for customers and shareholders alike. The next 6–12 months will reveal how well these strategies translate into sustained growth in a world where inflation trends remain in flux but increasingly predictable on the margins.

The data remain a reminder that inflation is not a monolith; it is a mosaic of moving parts across goods, services, energy, and housing. For technology leaders, turning the January 2026 inflation signal into disciplined pricing, smarter investments, and customer-focused value will be the differentiator in a market that rewards clarity, efficiency, and measurable outcomes.